Synthetic identity fraud is the fastest-growing type of financial crime in the U.S., often goes undetected, and costs financial institutions an estimated $2B a year in losses.

Technically, there are two types of synthetic fraud, one where someone manipulates their identity, and another where identity is totally fabricated. In its simplest form, a synthetic identity is one where the name, date of birth, and social security number don’t correspond to any real person. That synthetic identity can then be used to apply for credit, just as any other person would.

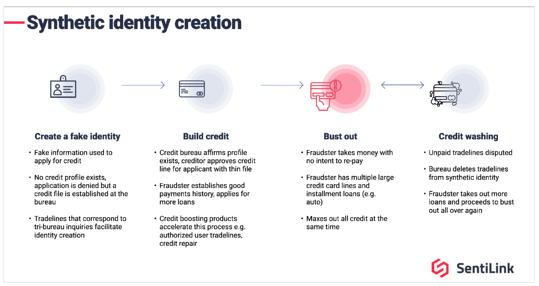

How do you create a synthetic identity?

Synthetic identities are surprisingly easy to create. It’s as easy as taking your own name, date of birth, and any nine-digit number that looks like a Social Security number and applying for a loan. While you will get declined for that initial loan, the act of applying for credit will create a record at the credit bureau with that name, date of birth, and made-up Social Security number. That newly created record is a synthetic identity.

With this newly minted synthetic identity, there are a variety of ways to build credit. The traditional way is to prove creditworthiness over a long period of time. It may involve applying for a $500 secured line of credit, and paying it off. Then apply for a $500 line of unsecured credit and pay it off. Then apply for a $1,000 line of unsecured credit and pay it off. And so on. It could take years to increase the credit score on this synthetic identity to the 700 to 750 range to be approved for much higher lines of credit.

Or, there are a variety of shortcuts. One is authorized user tradelines. These have been available on credit cards for a long time. It’s common for parents to list their teenage kids as authorized users on their credit cards so their kids can have access to higher credit lines and lower pricing.

With the rise in authorized user tradeline marketplaces, however, there’s no need to rely on a family member or friend to become an authorized user. There are countless marketplaces online now where you can pay a stranger to become an authorized user on their credit card. Tradelinesupply.com, Credit Patchup, Boostcredit101, Coast to Coast Tradelines, Personal Tradelines, and Credit Pro are just a few examples.

Non-reputable credit repair agencies are another tactic fraudsters use to increase the credit score on their synthetic identities. There are a host of companies that are magnets for fraudsters looking to quickly season their synthetic identities. They look like online retailers but are actually a type of credit repair agency. AG Jewelry is one example. They appear to be an online jewelry store, but, in reality, offer a $10,000 unsecured line of credit to anyone who applies. They even admit in writing that they “don’t do a soft or a hard credit pull” of anyone who applies, which essentially means that nearly anyone who applies is likely to get approved. They are, in effect, enabling fraudsters to buy tradelines in order to boost their score and look more creditworthy to other financial institutions. Once the synthetic identity has a high credit score, fraudsters apply for loans at legitimate lenders that they never repay, or “bust out.” After busting out, the boldest fraudsters then engage in credit washing.

Credit washing is a related form of fraud where an individual removes derogatory information from their credit report by lying about being the victim of identity theft. After doing so, their credit score can jump 200-300 points, so they can then trick lenders into issuing them credit that the lender never would have provided to somebody with as many missed payments, charge-offs, or other negative information.

4 Phases of Synthetic Identity Creation

In sum, there are four phases to synthetic identity creation. There’s the process to create the fake identity, then a period to build credit, followed by the bust out phase once the credit score has increased enough so the fraudster can get approved for several high dollar loans or credit cards (and not pay them back). The culmination is the credit washing phase where the fraudster claims to be the victim of identity theft so they can get the chargedoff tradelines deleted from their credit report, and they can use that synthetic identity all over again to apply for credit.

How do you identify a fake identity?

Identifying a fake or synthetic identity is tricky because a synthetic identity allows a criminal to circumvent the identity controls implemented in response to banking laws governing U.S. financial institutions. Most financial institutions follow Know Your Customer guidelines which simply require them to match the name, address, DOB, and SSN on an application with a record at the credit bureau. As demonstrated above, establishing a new record at the credit bureau is an incredibly simple process, so KYC solutions and processes can’t detect synthetic identities.

Identifying a synthetic identity requires data and insight to determine if the SSN provided belongs to a given name and DOB combination.

SentiLink, for example, provides a score that indicates the likelihood an incoming application is using a synthetic identity.

How does synthetic identity fraud work?

Once a synthetic identity is created, it can be used to open all sorts of financial accounts from checking accounts to credit cards, auto loans, personal loans and much more. For example, SentiLink found that one in five synthetic identities has an auto loan, and, one in seven synthetic identities has a loan from a credit union. Even niche players in financial services like patient finance lenders have to defend against synthetic identities. Synthetic identities were used to obtain fraudulent PPP loans, and synthetic identities were used to obtain EIDL Loans during the COVID-19 government relief efforts.

How to reject an application that’s likely using a synthetic identity

If you suspect someone is using a synthetic identity, one of the best ways to know for sure is to submit the name, DOB, and SSN combination through eCBSV or electronic Consent Based Social Security number verification. It’s a real-time service offered by the Social Security Administration that indicates whether the credentials provided match with what’s in their database. Since the SSA issues all SSN’s in the U.S., they are the single source of truth for this information. eCBSV is the most efficient, low cost way to reject synthetic identities in an FCRA compliant way.

Bio: Max Blumenfeld is the Co-founder and COO of SentiLink. Prior to SentiLink, Max led Risk Operations and Fraud Data Science at Affirm. Max holds a degree in mathematics and economics from the University of Chicago and was named to Forbes’ 30 Under 30 list in 2020.Charlie